Image From : gemini.google.com

In 2026, the health insurance landscape has shifted significantly.1 While federal laws have removed some of the most predatory practices—like “lifetime limits” on essential care—insurers have become much more sophisticated in how they use “the fine print” to cap their financial exposure.

If you are enrolling for the 2026 plan year, here are the hidden boundaries insurance companies rarely highlight in their marketing.

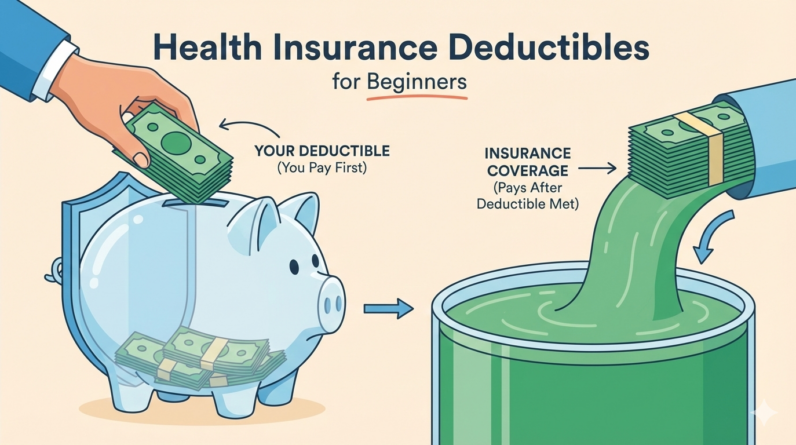

1. The “Out-of-Pocket” Trap: It’s Higher Than Ever2

Insurance companies love to advertise their “Out-of-Pocket Maximum” as your ultimate safety net. However, for 2026, that net has been moved much further down the cliff.

-

The 2026 Caps: The federal limit for out-of-pocket maximums has jumped to $10,600 for individuals and $21,200 for families.3 This is a nearly 15% increase from just a year ago.4

-

What they don’t tell you: This limit only applies to “Essential Health Benefits” provided by “In-Network” doctors.5 If you receive a life-saving treatment that isn’t on the EHB list, or if a specialist in your “In-Network” hospital is actually “Out-of-Network,” you could owe tens of thousands above that $10,600 cap.

2. The “Medical Necessity” Veto

In 2026, insurers are increasingly using AI algorithms to deny claims based on “Medical Necessity.”

-

The Secret: Your doctor might say you need a specific surgery or a new weight-loss medication (like the newly covered Part D anti-obesity drugs), but the insurance company’s AI might disagree.

-

The Limit: They don’t “limit” the coverage in writing; they simply refuse to authorize it, effectively placing a $0 limit on that specific treatment. Always check your plan’s “Prior Authorization” list before scheduling procedures.

3. Hidden “Sub-Limits” on Care6

While a plan might say it has “Unlimited Sum Insured,” the fine print often contains sub-limits that cap specific types of expenses.7

-

Room Rent Caps: Many plans limit how much they will pay for a hospital room per day (e.g., $500/day).8 If the hospital charges $800, you pay the $300 difference.

-

Proportional Deductions: This is the most dangerous hidden clause. If you exceed your room rent limit, some insurers will proportionally reduce their coverage for everything else—including surgery and doctor fees—leaving you with a massive bill.9

4. The 2026 “Co-Payment” Mandates

New regulations in several regions (and certain US private plans) now mandate a minimum co-payment even for high-tier plans.

-

The Rule: Some 2026 policies now require participants to pay at least 10% of every claim cost, regardless of whether you’ve met your deductible.

-

The Impact: This effectively acts as a “coverage floor,” ensuring you are never truly 100% covered, even for catastrophic events.

Key Coverage Limits to Watch in 2026

| Limit Type | The “Marketing” Version | The 2026 Reality |

| Out-of-Pocket Max | “Your total financial risk is capped.” | $10,600 (Individual); excludes out-of-network. |

| Medicare Part D | “Unlimited prescription coverage.” | Annual cap is $2,100 for covered drugs only. |

| Catastrophic Plans | “Cheap emergency coverage.” | Now eligible for HSAs, but have massive deductibles. |

| Gender-Affirming Care | “Comprehensive coverage.” | Marketplaces are no longer required to cover this in 2026. |