Image From : gemini.google.com

Understanding your health insurance deductible is the single most important step in managing your healthcare costs. In 2026, deductibles have become higher and more complex, often acting as the “gatekeeper” to your insurance benefits.

Here is a simplified guide to how they work and what you need to watch out for this year.

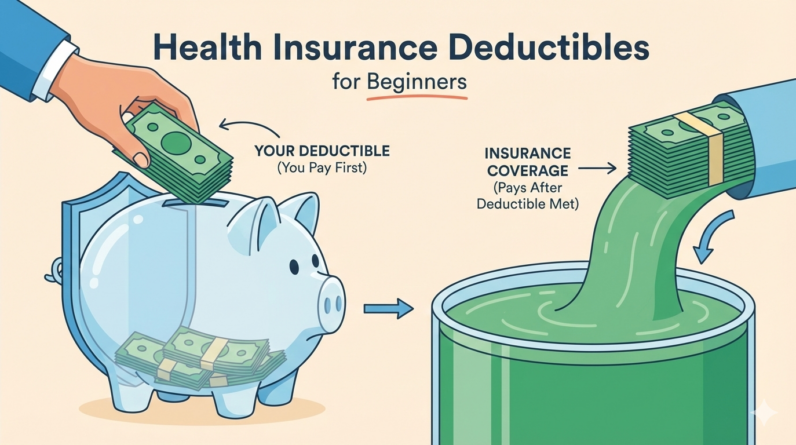

1. What is a Deductible?

A deductible is the fixed amount of money you must pay out-of-pocket for covered medical services before your insurance company begins to pay its share.

-

Example: If your deductible is $2,000, and you have a surgery that costs $5,000, you pay the first $2,000 yourself. After that, your insurance “kicks in” to help cover the remaining $3,000.

-

The Reset: Most deductibles reset to zero every year on January 1st. Even if you met your deductible in December, you start over in the new year.

2. The 2026 “Free” Services (The Exception)

Even if you haven’t paid a penny toward your deductible, most 2026 plans are required to cover Preventive Care at 100% cost to them. This typically includes:

-

Annual physical exams and well-child visits.

-

Standard immunizations and flu shots.

-

Screenings for blood pressure, cholesterol, and certain cancers.

Tip: Always check if a service is “Preventive” before you go. If you discuss a new health problem during a “free” checkup, the doctor may bill it as a diagnostic visit, which will count toward your deductible.

3. Individual vs. Family Deductibles

If you are on a family plan, you likely have two different numbers to track:

-

Individual Deductible: Once one person hits this amount, the insurance starts paying for them specifically.

-

Family Deductible: Once the total spending of all family members combined hits this amount, the insurance starts paying for everyone on the plan.

4. Choosing Your Strategy for 2026

In the current market, you generally have two choices. Your decision should be based on your health and your “rainy day” savings.

| Plan Type | Premium (Monthly Cost) | Deductible (Pay when sick) | Best For… |

| High Deductible (HDHP) | Low | High ($1,700+) | Healthy people who want to save money and use an HSA. |

| Low Deductible | High | Low (Under $1,000) | People with chronic conditions or those who visit doctors often. |

5. Common Deductible “Pitfalls”

-

Premiums don’t count: The monthly bill you pay to keep your insurance active does not count toward your deductible.

-

Out-of-Network: If you see a doctor who isn’t in your plan’s network, that money often won’t count toward your “In-Network” deductible at all.

-

Pharmacy Deductibles: Some 2026 plans have a separate deductible for prescriptions. You might meet your medical deductible but still have to pay full price for your meds until your pharmacy deductible is met.